As the cost of higher education rises, schools and skills training programs are seeking new financing options to offer their students. Income Share Agreements (ISAs) are one method winning the attention of investors and education providers alike.

As the cost of higher education rises, schools and skills training programs are seeking new financing options to offer their students. Income Share Agreements (ISAs) are one method winning the attention of investors and education providers alike.

It’s no secret that student loan debt is a problem, not only for those who bear their burden but for society as a whole. In 2022, the amount of student debt in the United States was estimated at $1.75 trillion.

Income Share Agreements (ISA) have entered the market as an alternative to traditional private student loans. Under an ISA contract, you are provided with a deferred tuition option to cover costs in exchange for a promise to pay a fixed percentage of your future income after you’ve graduated.

Although Income Share Agreements aren’t for everyone, they do have many benefits that can prove helpful for both students and schools. Here are some of the benefits of having an Income Share Agreement program. First, let’s take a look at the benefits they have for schools and skills-training programs.

Income Share Agreements are great for those who want to attend classes but may not have the means to, or may not want to take out a traditional personal loan to access college.

Colleges, Universities, and boot camps alike are using Income Share Agreements to add more options to increase accessibility for students. Institutions implementing Income Share Agreements typically use them to fill funding gaps for students who have exhausted their financial aid options, or who may be debt-averse.

Income Share Agreements also assist those who cannot access federal financial aid, especially anyone attending alternative education, like coding boot camps. Students interested in boot camps or alternative programs can’t access federal financial aid since these programs are currently ineligible for Title IV funding.

David Barnett, executive vice president, and CFO at Bernau speaks on the benefits of ISAs at the university:

“With Income Share Agreements, Brenau students will have the freedom to pursue their academic interests; they just won’t have to worry about un-affordable student loan repayment or the other strains that come with traditional student loan debt.”

Related to point number one, another advantage of offering an Income Share Agreements as one of your financing options is that it fills empty seats that a school might otherwise not be able to fill through traditional educational financing. Because Income Share Agreements offer another financing option to students, some students who may not have otherwise considered attending due to the need to take out a student loan now have access to education. The built-in protections Income Share Agreements provide may also sway students who may have been on the fence about attending. Because Income Share Agreements increase accessibility to students, colleges are able to increase enrollment and fill empty seats.

Individuals interested in higher education may at times decide not to enroll due to uncertainty about the return on their investment in a student loan. Personal loan aversion can cause students to delay enrollment in higher education. With an Income Share Agreement, schools can offer an alternative financing option to those who may be hesitant to take out a personal loan.

With many traditional student loans, the student takes on almost all the risk of the debt. With an ISA program schools are able to confidently signal to students that the skills the student will learn through their program will allow them to find a job in their field, or gain enough skills to find another suitable position. This also adds to the school’s credibility and shows they are willing to share the risks and rewards with the student.

Right now, students bear all the burden of traditional student loans. If students drop out or receive an education that does not prepare them for the workforce, the student is responsible for payments regardless of their job situation. ISAs work and change that model and allow students and schools to better share in the risks and rewards of educational financing.

With Income Share Agreements, colleges will want to offer programs that are tailored to the needs of the modern-day workforce. This benefits both the student and the school. The student will be prepared for a great job, and the school will benefit because if the student succeeds then their Income Share Agreement program succeeds.

Income Share Agreements also benefit students in multiple different ways:

Although Income Share Agreement contract terms vary, most Income Share Agreements allow you to go through the program without worrying about paying for it until you have an income post-graduation. This helps students to focus on school and getting the education they need without having to make payments while studying or needing to have a large amount of money saved up before beginning their first semester. With an Income Share Agreement, you’ll only start making payments after you graduate and once you get a job, you usually do not owe anything until you earn over a certain amount. This means that you will only pay if your education leads to success in the job market.

Unlike with a traditional private student loan, you won’t have a fixed payment hanging over your head with an Income Share Agreement. Because an Income Share Agreement is linked to your pretax, monthly income by a fixed percentage, if your first job after your college education earns you less than the minimum income threshold, you won’t have to worry about making payments.

This is because ISAs typically have something called a Minimum Income Threshold that you have to meet before payments start. If your income ever drops below that point, your payments are paused until you are earning above that threshold. Your payments aren’t due if you lose your job, after all, you can’t owe a percentage of your income if you have no income. This additional flexibility is a great benefit of Income Share Agreements.

Income Share Agreements also have a maximum payment cap which limits your total financial commitment. The max payment cap is the absolute maximum payment you could pay towards your Income Share Agreement obligation. Your total payments will never exceed this cap and if you do reach the cap on your payments, your Income Share Agreement obligations are done!

As described above, the consumer benefits included with an Income Share Agreement are there to assist students during their repayment period and help to remove compounding interest that seems to never disappear.

ISAs offset risks for students because they have the potential to protect students from paying for educational experiences that don’t create value for them in the labor market. Income Share Agreements help to shift the risk of poor workforce outcomes away from students and to produce better outcomes by helping to balance out the risks associated with educational financing. In the future, ISAs can potentially help change how education providers keep their curriculum relevant and up to date with the current workforce, so students can enter the workforce effectively.

Our private student loan system needs to be fixed. Income Share Agreements offer students an alternative to private student loans creating compounding debt for them. Schools and students are beginning to see the benefits of Income Share Agreements.

Are you a school or skills-training program looking to offer your own Income Share Agreement program? Book a meeting with a member of the Meratas Partner Team today!

Are you a student looking to level up your career with an Income Share Agreement? Check out our student page to find the best program for you!

(more…)At Meratas, we believe Income Share Agreements (ISA) are part of the solution to the current educational financing. Though still a newer concept, Income Share Agreements have become an educational finance alternative to traditional private student loans. If you aren’t familiar with them, an Income Share Agreement typically grants a deferred tuition option in exchange for a percentage of the student’s pre-tax income after graduation.

As more students are concerned about how they will afford traditional loan repayments, schools and programs are beginning to think of different ways to finance the cost of tuition. Income Share Agreements can be an excellent alternative for students.

(more…)Student debt has become a serious problem in the United States. Income Share Agreements (ISA) are a promising alternative to personal student loans. Unlike traditional loans, they don’t accrue interest and there is no principle that is paid down.

Looking to make a career switch and break into the world of tech? One popular way to jump-start a lucrative career in web or software development is a coding bootcamp.

(more…)The price of tuition is still rising, and outstanding debt continues to go up every year. At 1.6 trillion outstanding loan debt in the United states has become the second highest source of household debt in the country. Income Share Agreements (ISAs) are being used as an alternative to traditional student loans and provide a promising solution to the crisis.

What if there was a way to make it so that you only pay for your education if it resulted in a great job?

Historically, financing options like traditional private loans have been the primary method of paying for coding bootcamps, colleges, and other educational institutions. However, recently, student debt has reached a crisis level—around $1.6 trillion in student debt is owed in the United States. The amount of people relying on these traditional loans to finance their education is increasing every year, and part of the solution to this problem is Income Share Agreements.

An Income Share Agreement (also called “ISA”), may at first appear unfamiliar but is rather straightforward. At the most basic level, they work like this: an ISA-funder or school provides a student with money to be used towards tuition or school/living expenses. In exchange, the student agrees to pay back a small percentage of their future earnings after they graduate and once they get a job. With an ISA if you make less than a certain amount (the payment floor) you don’t make payments. Since the amount repaid is linked to the student’s earnings, if the student ends up in a low paying job, then the amount paid back may be less than the amount received. If, however, the student works towards a high-paying career, the amount paid back is still limited by a “ceiling” for further protection.

Income Share Agreements aligns risk and reward between student and school, by removing the upfront financial commitment required to pursue education. It’s like going to school with no upfront payments, and then only paying for the degree if it actually helps you get a better job. Because of this, ISAs align the risk and rewards and incentivize students, schools, and funders to work together to promote and fund only the best programs that lead to solid careers.

Since there may be uncertainty at this time around income and job prospects, this innovative financing option provides the flexibility students need as their interests, passions, jobs, and the workforce change. Payments may be paused for students pursuing graduate degrees, engaged in voluntary service, and working full-time, and making less than the payment floor.

Because of these upside and downside protections, an ISA is a great alternative to private loans and a great way to cover any remaining expenses after you’ve exhausted all scholarships and grants.

This brief introduction to Income Share Agreements will cover several things you should know about ISAs, including the following:

Traditional personal loans contain a principal balance plus interest, both of which typically must be repaid irrespective of your circumstances. This means, with a personal loan, you will pay back more than the amount you borrowed.

With most personal loans, interest continues to accrue during your grace period and any temporary deferment. This accrued interest is added to the principal balance you must repay. When this happens, the amount you are obligated to repay has actually grown despite whether your loan is in deferment. This is called “negative amortization” and is a hidden cost leaving many borrowers in a much worse position than when they originally took out their loans.

Since ISAs have no principal balance that must be repaid, there is absolutely no risk of negative amortization. With an Income Share Agreement, the money you receive represents an investment in your future success, in exchange for which, you promise to share a small portion of your future income with your funder. So, depending on your future employment, the amount you share may be more or less than the amount you received. The fact that you may lawfully pay back less than you received is a key benefit of Income Share Agreements when compared to traditional personal loans.

With an Income Share Agreement, the ISA-funder is literally making an investment in you. The funder is betting on your future success once you’ve finished your studies. This is why ISA-funders must carefully vet those in whom they invest, and also why ISA-funders will help their students with mentoring, career advice, and networking opportunities; all to ensure their students obtain a lucrative career.

Since Income Share Agreements work differently from traditional private loans, you’ll want to familiarize yourself with ISA terms, such as:

Income Share Percentage (or Income Share): This is the fixed percentage of your monthly pre-tax income that you agree to share during your contract term. Depending on your ISA and program, Income Shares can range from 2.50% to as high as 17.50%.

Monthly Payment: This is what you pay back on a monthly basis after you’ve graduated during the term of your ISA contract. To put some numbers to this, if your Income Share is 5%, and you’re earning $60,000 per year (or $5,000/month), your Monthly Payment would be $250/month (i.e., your income share (.05) multiplied by your monthly income ($5,000) = $250).

Minimum Threshold (or “Floor”): The Floor protects you from making payments whenever you are earning less than expected based on your degree and career. If your monthly income is under your Floor, your payments are automatically suspended. So, for example, if your Floor is $50,000 your monthly payments will be automatically waived whenever you are earning less than $50,000/year (or $4,166/month).

Payment Cap (or “Ceiling”): The Payment Cap represents the most you might ever need to pay, in a high earning career. ISAs come with a limit (or ceiling) on what they can charge you over the life of the contract. Should you ever reach your ceiling, then your contract will automatically terminate, even if sooner than the full contract term.

Automatic Deferment: During periods of involuntary unemployment, under-employment, or if you are unable to work due to serious illness, your payment obligations will be automatically waived without penalty. Unlike traditional loans, where you must apply for temporary deferment, with an ISA, your payments will be suspended automatically during periods of economic hardship.

Contract Term: The contract term in an ISA is how long your payment obligations will last. Some ISAs require a fixed number of payments (an exact number, like 48 or 60), others have a fixed contract term (48 or 60 months). With the latter, you contract keeps counting down even if you’re in deferment, meaning you ultimately may not have to pay as much-however, it’s important to read your contract terms as some types of deferment (i.e., if you voluntarily quit your job to travel the world) may extend your contract term.

If you want an alternative financing method with built-in downside protection and no compounding interest, you should consider an ISA. Most importantly, an ISA is a balanced financing method that protects the student and rewards the school for empowering students to realize their potential.

Perhaps the most prominent coding bootcamp income share agreement is through Lambda School. Lambda School provides students with high-quality, nine-month courses in various areas like iOS development and full-stack web development. Further, they offer students hands-on career support to help them get hired. In exchange, students agree to pay back 17 percent of their income for the first two years they are employed—but only if they earn over $50,000 per year. If a student is really successful after graduation, the maximum they will ever pay is $30,000, after which their ISA will be complete.

Other prominent ISA programs include those offered by Kenzie Academy, Flatiron School, Make School, Thinkful, Northeastern, and Holberton School.

In 2016, Indiana’s Purdue University launched their “Back a Boiler” ISA fund. It allows students to borrow the money they need for college in exchange for a percentage of their future income. Students of any major can agree to share between 1.73 percent and 5 percent of their monthly income over a period of time in exchange for the money they need to finance their education. Students can borrow $10,000 per year, but they will pay back no more than 2.5 times the initial amount borrowed. Lackawanna College, Messiah College, and the University of Utah are among dozens of other universities currently exploring income share agreements.

If you’re unmoved by existing income share agreement providers, you could always take on the challenge of convincing your school to start its own program. That’s where Meratas comes in.

Meratas provides a full-service SaaS Platform for Schools and Skills-Training Courses to design, administer, and service custom ISA programs. We help institutions create impactful ISA programs designed to promote student accessibility and increase enrollment.

Our programs are intended to incentivize students, schools, and capital providers to work together to promote and finance only the best educational programs that lead to more successful careers.

We hope this has helped you shed some light on Income Share Agreements as an alternative to traditional private student loans. Want to learn more about ISAs and dive a little deeper? Check out our ultimate guide to Income Share Agreements here!

If you’re interested in offering an ISA option at your school or program you can schedule a call with one of our ISA specialists here! If you’re a student and think your school or program should offer an ISA option let us know here!

Student debt is a significant problem, outstanding student loan debt in the United States is at around $1.75 trillion as of 2022 the second highest source of household debt in the country, and it continues to go up each year.

Income-share agreements have emerged as a financing option for colleges and education programs. They’ve proven to be a more student-friendly form of financing.

An Income Share Agreement works differently than traditional private student loans; students don’t have to worry about paying back a principle or mounting interest. Besides the absence of growing interest and generally, no upfront payments, a significant benefit of Income Share Agreements is the fact that there are certain instances when your payments are paused or deferred.

ISAs keep students from paying for educational experiences that don’t create value for them in the labor market, aligning the risk and rewards of education and creating better outcomes.

Because of how different ISAs are in regard to repayment, it’s important to educate students on the different ways to pay back their ISA. We have a whole guide on how to finish paying an ISA. After reading this post, if you have any other questions about Income Share Agreements, check out our ISA page.

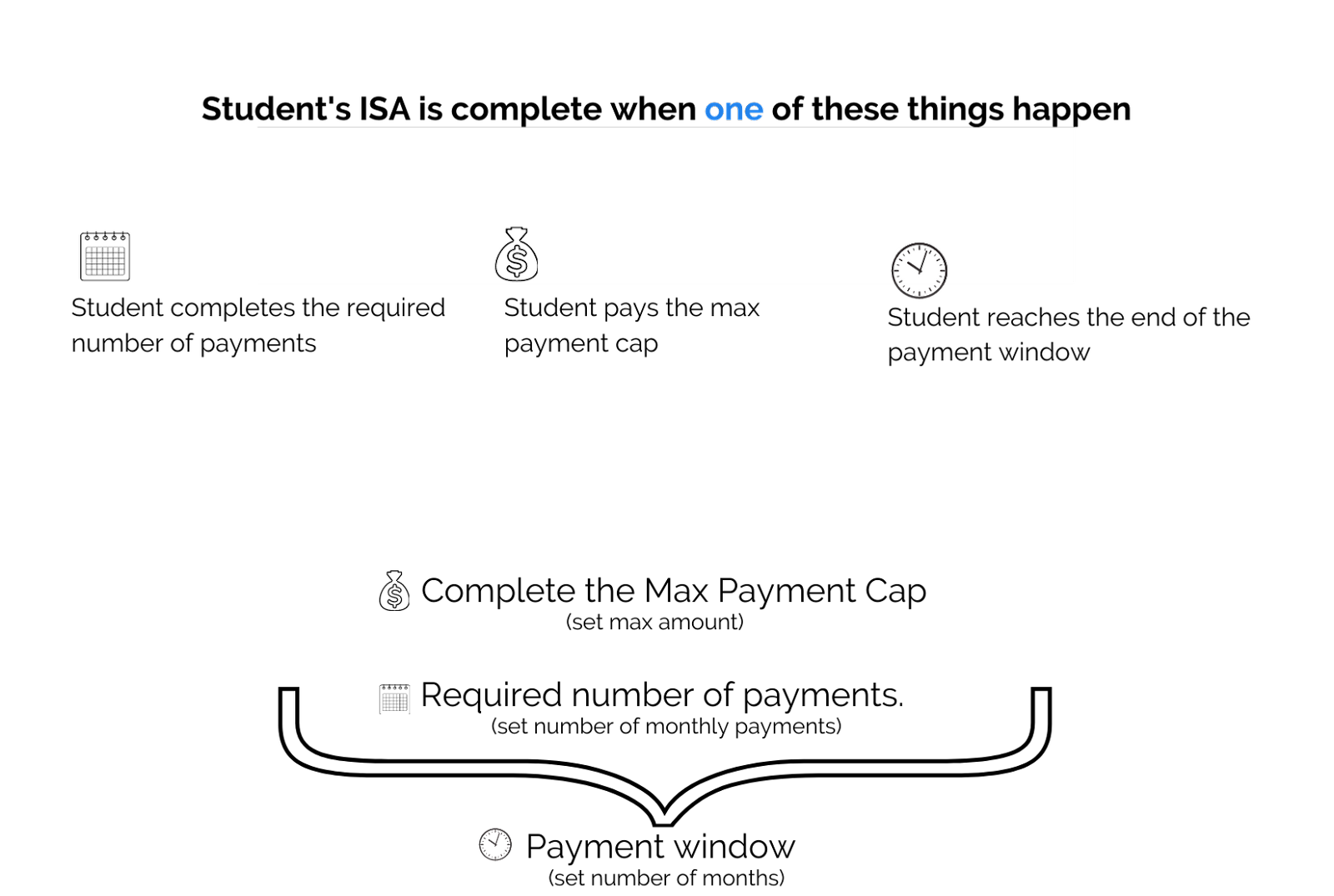

There are three different ways to finish your ISA. Required Payments, Payment Cap, and Payment Window. In this blog post, we’ll be covering the third way you can finish your ISA:

One way to satisfy your ISA is by reaching the end of the Payment Window. Before we go any further it’s important to know that the most common way to satisfy one’s ISA obligation is to make the required number of monthly payments. With an ISA, you pay back a percentage of your earnings each month for a set number of months. Each of these payments is considered one of your Required Payments. There’s also a Max Payment Cap, which is the most you could possibly ever pay towards your ISA. It is put in place to protect high earners from overpaying through the Required Payments.

The school or lender who you have an ISA with will have a set time period to collect your Required Payments or Max Payment Cap. This time period is called the Payment Window. However, if you have not reached either of those two and the Payment Window ends, you’re absolved of your ISA obligations.

This is a protection built into your ISA to help you in case you’re without a job for an extended period. For example, let’s say your ISA states the school has 48 months to collect your Required Payments or Max Payment Cap. Let’s say that 12 months into your ISA, you unfortunately become unwell. Consequently, you can no longer work. Let’s say again that you don’t end up getting work until month 45 of your ISA. You make a few more payments but then reach month 48.

Even though you only made 15 payments and didn’t pay back the entire Max Payment Cap, since the 48 months of your ISA Payment Window are up, your ISA is finished. This form of ISA termination is more on the rare side since it is less likely to be without work for a period that long but again, this is a built-in protection to ensure students aren’t making payments for several years or even decades after their program ends.

One thing to be aware of before you sign your ISA contract is that a payment window can, in some cases, be extended. This varies from ISA to ISA and is ultimately up to the school or lender the student has an ISA with on whether or not they want to include measures to extend the payment window. Be sure to read your contract carefully before signing so you are aware of how long you could potentially be paying back your ISA.

If you’ve ever wondered how to finish paying your ISA through the Payment Window, hopefully we’ve been able to answer all those questions! If you’re ready to jump into a new career using the power of an ISA, check out all the amazing online training programs that offer an ISA on our student’s page here! If you’re interested in offering an Income Share Agreement at your program click here to schedule a meeting with one of our ISA specialists.