College is far more expensive than it was a decade ago making it difficult for some to afford higher education. College still provides a strong return on investment for many students — but the risk profile of that investment has gone up dramatically. But we are starting to see a growing number of colleges and universities stepping up to share some of the risks and rewards with their students.

One way that schools are sharing the risk and reward of education with their students is through the use of Income Share Agreements (ISAs). These allow students to pay nothing upfront in exchange for a percentage of their gross income for a fixed time once they graduate and are employed making above a certain, agreed-upon income.

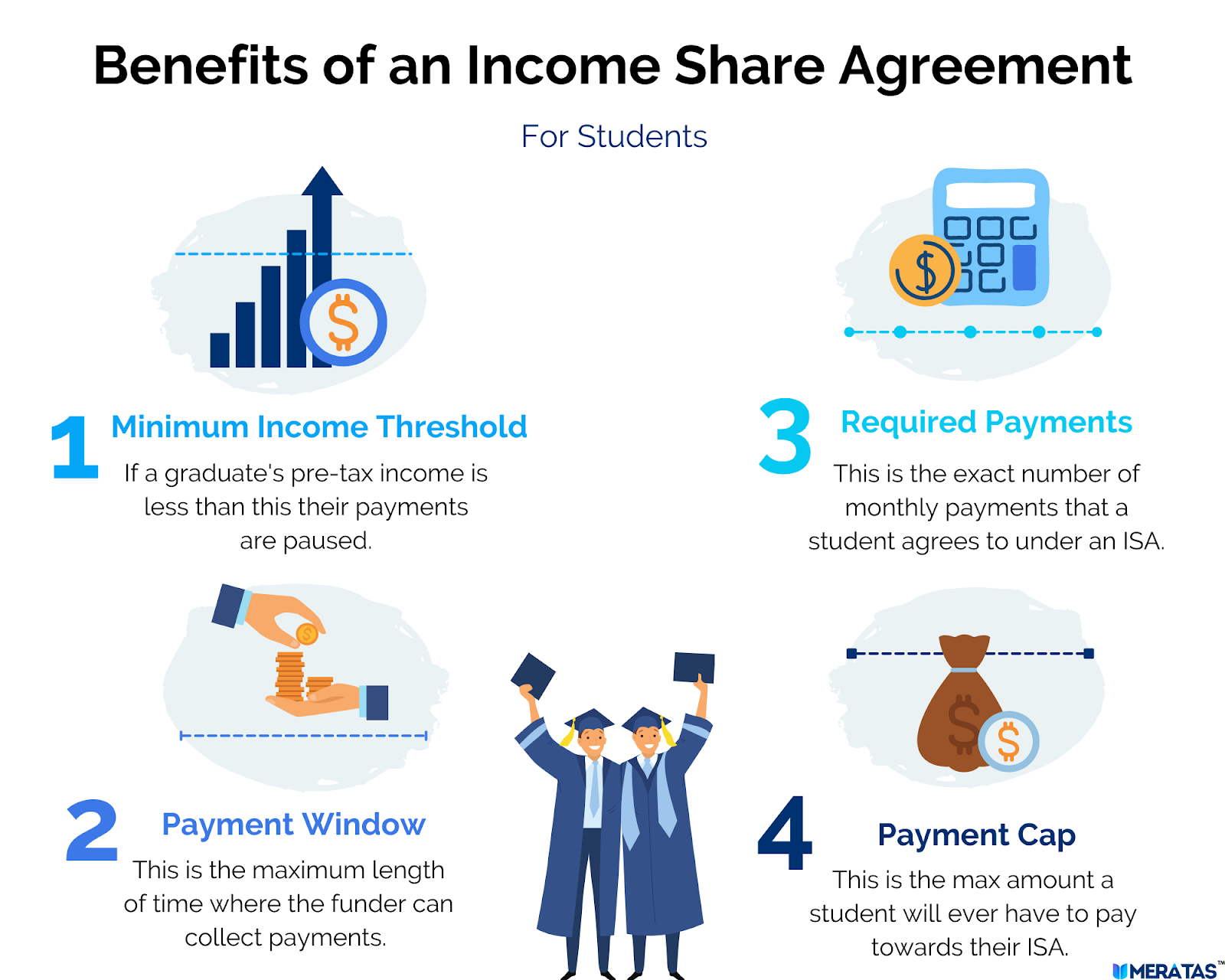

Income Share Agreements have a whole host of student benefits that are often absent from traditional private student loans. For example, there is something called the Minimum Income Floor, which is the minimum amount a student needs to earn before they begin paying back their ISA. There is also a payment window, which is the set time frame that the ISA funder has to collect all of the required payments under an ISA.

In today’s post, we’re going to take a look at the ISA student benefit known as the payment cap.

The Payment Cap

One way to satisfy your ISA is by paying the Max Payment Cap. (The most common way to pay back your ISA is by making all the required payments. Read about the different ways to pay off your ISA here) The payment cap is in place to ensure that high earners do not over-pay on their ISA.

The Max Payment Cap is built into your ISA and is the most you’ll ever need to pay towards your ISA. A Payment Cap is usually some amount more than the Funded Amount (the amount the school is fronting you for their program as part of your ISA). Once you hit your Max Payment Cap, your ISA is completed.

For example, let’s say your ISA terms dictate that you pay 10% of your monthly income over 24 required payments (read more about required payments here.) Your Max Payment Cap is $12,000. Based on your income, you would pay $500 per month to your ISA. If your income doesn’t change for 24 months and you make each of those $500 payments each of those months, your ISA would be finished. But let’s say, you’re crushing it at your job, and 10% of your income would now be $1,000 a month. If you had to make the same 24 repayments, you would pay double the amount over the course of your ISA.

If you pay your $1,000 payments each month, you’ll hit your payment cap in only 12 months thanks to the payment cap. You’ll pay it back a full year earlier than if you were making the 24 required payments!

The Incremental Payment Cap

The Maximum Payment Cap limits the maximum amount of income a high-earning student is required to share. Incremental Payment Caps give students even more options and benefits in paying off their ISA. Incremental Payment Caps are designed to reward students by providing an incrementally lower payment cap year over year for students to pay off their ISA at lower cap rather than letting the contract go full-term.

For example, if you sign an ISA to borrow $8,000 let’s say your Max Payment Cap is equal to $15,000. This is the normal payment cap, the most you would ever pay towards your ISA. But with an incremental payment cap, the payment cap would be lower in the first year and incrementally increase to the full cap over the course of four years. Let’s say that your payment cap for year one was also $8,000. That means, that if you made extra payments towards your ISA or earned enough to pay $8,000 towards your ISA in the first year, you would pay nothing more than the tuition amount! Can’t pay that $8,000 in the first year but still want to take advantage of the incremental payment cap? In this example, let’s say that the payment cap for year two is $10,000. This means if your total ISA payments reach $10,000 in those first two years, your ISA is still considered satisfied even if you haven’t reached the total payment cap of $15,000 or made all of the required payments.

The Incremental Payment Cap gives students incentive to pay off their ISA quicker instead of holding off on paying it down. The incremental payment cap will continue to get bigger over 4 years until it reaches the overall payment cap of $15,000.

Meratas is the only ISA platform that offers this student benefit as an option to partners on our platform and is one of the many benefits of working with Meratas for all of your ISA needs. If you’re interested in offering an Income Share Agreement at your program, click here to schedule a meeting with one of our ISA specialists.

Although every effort has been made to provide complete and accurate information, Meratas Inc. makes no warranties, express or implied, or representations as to the accuracy of content contained herein. Meratas Inc. assumes no liability or responsibility for any error or omissions in the information contained herein or the operation or use of these materials.

.png)